India's Digital Currency Revolution: BIMCOIN, Digital Rupee, and the Future of Payments

Updated on : 24 January, 2025

Image Source: observervoice.com

Table Of Contents

- 1. Overview of Digital Currency

- 2. BIMTECH to Launch BIMCOIN

- 3. What is Digital Rupee (e₹)?

- 4. History of Digital Currency in India

- 5. Objectives of Digital Rupee

- 6. Types of Central Bank Digital Currencies (CBDCs)

- 7. Issuance Mechanism of Digital Rupee

- 8. Technology Behind Digital Rupee

- 9. Advantages of Digital Rupee

- 10. Impact on Traditional Banking Systems

- 11. International Implications of CBDCs

- 12. Pilot Projects and Implementation Phases

- 13. Emerging Payment Trends in India (2025)

- 14. DigiDhan Mission and Its Impact

- 15. Conclusion

Table Of Contents

Overview of Digital Currency

Digital currency refers to any form of currency that exists exclusively in digital form, which includes various types such as cryptocurrencies (e.g., Bitcoin, Ethereum) and Central Bank Digital Currencies (CBDCs). Unlike physical cash, digital currencies are stored electronically and can be utilized for online transactions or transferred between users through digital wallets.

Importance of Digital Currency in India

In India, digital currency holds significant potential for transforming the financial landscape by enhancing financial inclusion, streamlining transactions, and driving economic growth. With a considerable portion of the population still unbanked or underbanked, adopting digital currencies can bridge this gap, providing access to essential financial services for millions.

BIMTECH to Launch BIMCOIN

Image Source: cdn.prod.website-files.com

Overview of BIMCOIN Initiative

The Birla Institute of Management Technology (BIMTECH) has recently launched a blockchain-based digital currency called BIMCOIN. This initiative aims to enhance financial transactions within its campus ecosystem by facilitating instant crypto transactions among students, vendors, and administrators. Additionally, BIMCOIN serves as a practical educational tool, offering students hands-on experience in blockchain technology and digital currencies.

BIMCOIN operates on a permissioned blockchain platform, ensuring secure transactions while promoting transparency and efficiency within campus operations. This initiative responds to the growing need for educational institutions to integrate modern financial technologies, preparing students for careers in the rapidly evolving fintech landscape.

Implications for the Indian Digital Currency Landscape

The launch of BIMCOIN signifies a notable shift towards integrating digital currencies into everyday life in India, particularly within educational institutions. This initiative could inspire other universities to adopt similar models, fostering a culture of innovation and technological adoption across the country.

As cryptocurrencies gain legitimacy globally, initiatives like BIMCOIN may pave the way for broader acceptance and regulatory frameworks surrounding digital currencies in India, encouraging more institutions to explore the potential of blockchain technology.

What is Digital Rupee (e₹)?

Image Source: bizzbuzz.news

Definition and Characteristics

The Digital Rupee (e₹) is India's proposed Central Bank Digital Currency (CBDC), designed to complement physical cash while leveraging the benefits of digital technology. It aims to provide a secure and efficient means for conducting transactions while maintaining the stability associated with traditional fiat currencies.

Key Characteristics:

- Legally recognized as tender: The Digital Rupee is acknowledged as a valid form of payment.

- High security: It employs advanced encryption methods to ensure transaction safety.

- Accessibility: The Digital Rupee can be accessed through various digital platforms, facilitating ease of use.

Legal Status and Recognition

The legal framework governing the Digital Rupee is crucial for its acceptance within the financial system. As a state-backed currency issued by the Reserve Bank of India (RBI), it will be recognized by financial institutions and regulatory bodies, ensuring its legitimacy in transactions across various sectors. This framework fosters trust and encourages widespread adoption among users.

Popular Blogs

ICC Champions Trophy 2025: Schedule, Teams, Venues & More

on December 25, 2024

World Test Championship 2024-25 Points Table

on December 24, 2024

Aus vs Ind: Border-Gavaskar Trophy 2024 – History & Key Fixtures

on December 14, 2024

Gukesh Dommaraju: Youngest Chess World Champion at 18 Years

on December 13, 2024

GRAP 4 Restrictions in Delhi-NCR: What's Open and Shut?

on December 17, 2024

Russia’s mRNA Cancer Vaccine: A Groundbreaking Step in Oncology

on January 09, 2025

Lulu Mall in India - Complete List of Lulu Malls, and Key Facts

on December 26, 2024

History of Digital Currency in India

Image Source: scroll.in

Initial Proposals and Recommendations

India's journey toward adopting digital currency began with discussions on the potential impact of cryptocurrencies on the economy. Initial proposals suggested exploring Central Bank Digital Currencies (CBDCs) as a means to modernize the financial system while addressing concerns related to cryptocurrencies. In 2017, a high-level inter-ministerial committee was formed to study the governance and usage of virtual currencies, recommending the development of a digital form of fiat currency using Distributed Ledger Technology (DLT). This laid the groundwork for future CBDC initiatives, despite the lack of official recognition for cryptocurrencies at that time.

Development Timeline

Significant milestones in the development of digital currency in India include:

- Formation of Committees: The establishment of committees to study CBDCs and their implications for the financial ecosystem.

- Regulatory Sandbox: On 16 December 2020, the Reserve Bank of India (RBI) announced a regulatory sandbox to test next-generation technologies for cross-border payments, collecting data on benefits and risks.

- Proposed Legislation: On 29 January 2021, the Indian Government proposed a bill to ban trading in cryptocurrencies while empowering the RBI to develop a programmable digital rupee.

- Pilot Projects: The first pilot for the Digital Rupee - Wholesale (e₹-W) was launched on 1 November 2022, followed by the pilot for retail digital rupee (e₹-R) on 1 December 2022. These pilots aimed to test real-world applications and refine the operational framework.

Objectives of Digital Rupee

Image Source: licdn.com

Financial Inclusion Goals

One primary objective of the Digital Rupee (e₹) is to promote financial inclusion by providing unbanked populations access to banking services through mobile devices and digital platforms. This initiative aims to bridge the gap for those without access to traditional banking, allowing them to participate in the formal economy and utilize essential financial services.

Enhancing Transaction Efficiency

The Digital Rupee seeks to streamline payment processes, reducing transaction times and costs associated with traditional banking methods. By leveraging digital technology, it aims to facilitate faster and more secure transactions, ultimately increasing economic activity. The introduction of e₹ is expected to lower transaction costs for both domestic and international money transfers, making financial transactions more efficient and accessible for all users.

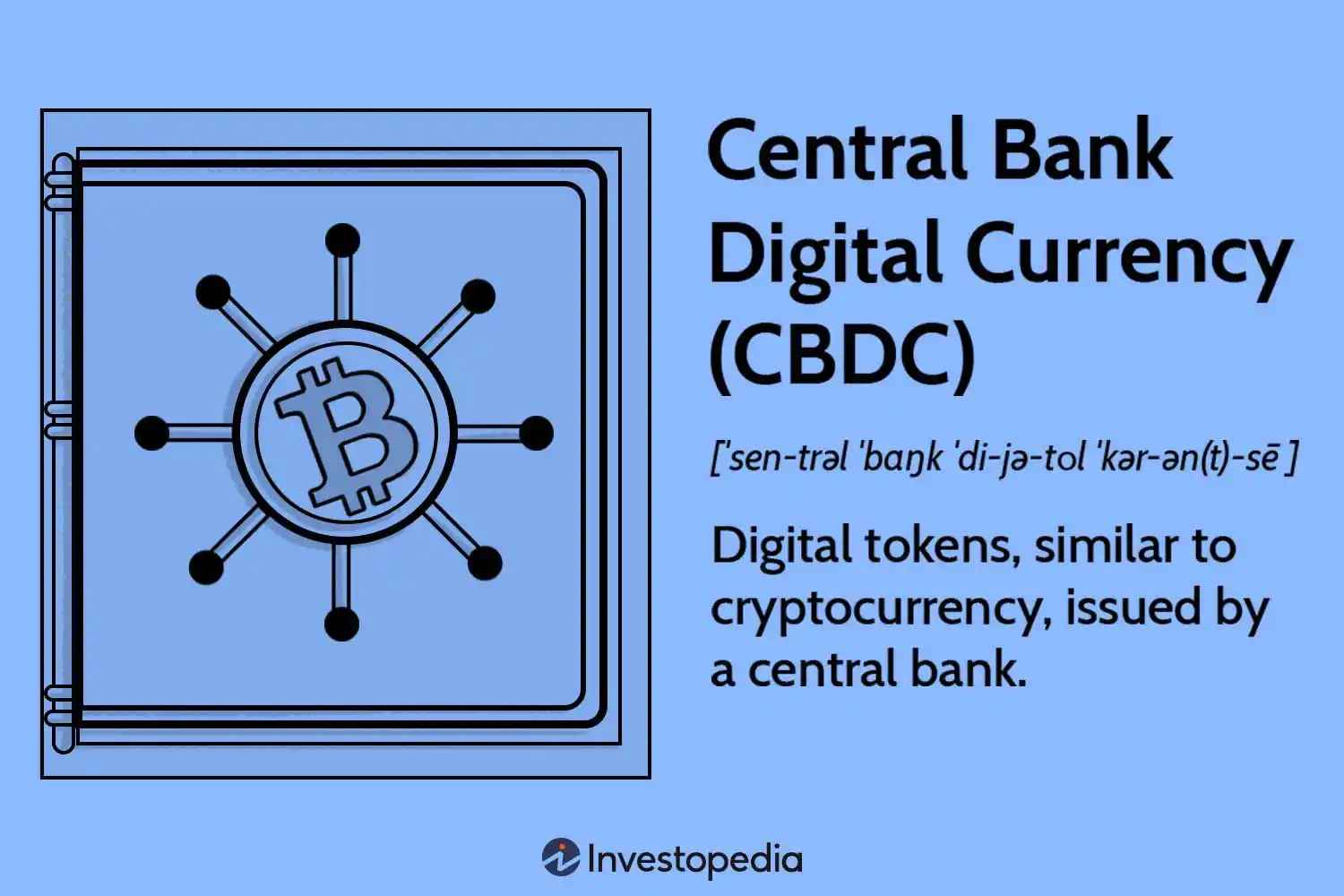

Types of Central Bank Digital Currencies (CBDCs)

Image Source: investopedia.com

Central Bank Digital Currencies (CBDCs) can be categorized into two primary types:

Retail CBDC

- Definition: Retail CBDCs are designed for general public use, allowing households and businesses to make everyday transactions.

- Accessibility: They can be accessed through digital wallets, smartphone apps, or other payment systems, making them widely available for daily financial activities.

- Characteristics: Retail CBDCs may be further divided into:

- Token-based: Allow for anonymous transactions using private and public keys.

- Account-based: Require digital identification for access and transactions.

Wholesale CBDC

- Definition: Wholesale CBDCs are intended for use between financial institutions, such as banks, and are not accessible to the general public.

- Purpose: They facilitate high-volume, high-value transactions, including interbank transfers and securities settlements. This type of CBDC is particularly useful for improving the efficiency of the financial system.

Use Cases for Each Type of Central Bank Digital Currency (CBDC)

Retail CBDC Use Cases

- Consumer Payments: Retail CBDCs can facilitate everyday transactions between consumers and businesses, akin to using digital cash. This includes payments at shops, restaurants, and online platforms, enhancing convenience and accessibility for users.

- Financial Inclusion: By providing a secure and accessible digital payment solution, retail CBDCs can bridge the gap for unbanked or underbanked populations, empowering them to participate in the formal economy.

- Government Benefits Distribution: Retail CBDCs can be used to disburse social welfare benefits directly to citizens' digital wallets, improving transparency and reducing administrative costs.

- E-commerce Transactions: They enable seamless online payments, stimulating growth in e-commerce by offering merchants and consumers a secure, low-cost payment method.

Wholesale CBDC Use Cases

- Liquidity Management: Wholesale CBDCs enhance liquidity management among banks by providing a digital representation of existing reserves at the central bank, facilitating real-time gross settlement payments.

- Interbank Settlements: They are designed for interbank transactions, improving the efficiency of settlements between financial institutions and reducing counterparty risk.

- Cross-Border Payments: Wholesale CBDCs can streamline cross-border remittances and capital market transactions, making existing payment processes more efficient.

- Conditional Payments: They support conditionality in payments, allowing settlements to be dependent on the completion of another transaction or delivery of an asset.

Issuance Mechanism of Digital Rupee

Role of the Reserve Bank of India (RBI)

The Reserve Bank of India (RBI) plays a central role in the issuance and regulation of the Digital Rupee (e₹), ensuring its stability within the financial system. As the sole issuer, the RBI is responsible for maintaining the integrity and trust associated with this digital currency, similar to its role with physical cash. The RBI's oversight includes establishing the framework for the Digital Rupee, ensuring compliance with financial regulations, and addressing concerns related to security and privacy in transactions.

Distribution Process to Commercial Banks

The distribution mechanism for the Digital Rupee involves transferring e₹ through commercial banks, which will facilitate its circulation among consumers and businesses. This process is designed to ensure that the Digital Rupee is easily accessible to users while maintaining a direct connection to traditional banking systems.

- Intermediaries: Commercial banks act as intermediaries in distributing e₹ to end-users, allowing customers to transact via digital wallets provided by these banks.

- Transaction Types: Users can engage in both Person-to-Person (P2P) and Person-to-Merchant (P2M) transactions using e₹, utilizing QR codes for payments at merchant locations.

- Pilot Programs: The RBI has initiated pilot programs for both retail and wholesale segments of the Digital Rupee, assessing its functionality and stability in real-world scenarios before a broader rollout.

Technology Behind Digital Rupee

Blockchain and Distributed Ledger Technology

The Digital Rupee (e₹) is fundamentally built on blockchain technology, which provides enhanced security, transparency, and efficiency in transactions. This technology allows for a decentralized ledger that records all transactions in real-time, ensuring that data is immutable and verifiable. The use of a token-based system further facilitates secure transfers, where a common public key initiates the transaction, and a private key verifies it, maintaining user confidentiality for smaller sums while ensuring compliance for larger transactions.

Security Features and Protocols

Security measures are paramount in protecting users' transactions from fraud or cyber threats. The Digital Rupee incorporates several robust security features, including:

- Encryption Protocols: These protocols safeguard transaction data, ensuring that sensitive information remains confidential during transfers.

- Multi-Factor Authentication (MFA): This adds an extra layer of security by requiring multiple forms of verification before a transaction can be completed.

- Continuous Monitoring: Ongoing surveillance of the network helps detect and respond to potential threats in real-time, enhancing the overall security framework.

Advantages of Digital Rupee

Image Source: bitcoin.com

Cost Reduction in Transactions

One significant advantage of the Digital Rupee (e₹) is the potential for savings from reduced transaction fees compared to traditional banking methods. By eliminating intermediaries and streamlining payment processes, the Digital Rupee can lower the costs associated with printing, distributing, and managing physical currency. This reduction in transaction costs can benefit consumers and businesses alike, making financial transactions more affordable and efficient.

Speed and Efficiency in Payments

The Digital Rupee promises faster transaction speeds, enabling real-time payments that enhance business operations. Transactions made with e₹ are settled almost instantly, significantly reducing processing delays often encountered with conventional banking systems. This speed not only improves the efficiency of everyday transactions but also facilitates quick settlements in larger financial operations, thereby supporting economic activity.

Impact on Traditional Banking Systems

Potential Disruption to Existing Banks

The introduction of the Digital Rupee (e₹) may significantly disrupt traditional banking operations by altering how banks interact with customers. As e₹ facilitates direct transactions between users and the central bank, it could reduce the reliance on commercial banks for everyday banking services. This shift might lead to increased competition from non-bank financial institutions and fintech startups that offer digital payment solutions, potentially diminishing the role of traditional banks in payment processing and customer service. Additionally, as the demand for physical cash decreases, banks may need to adapt their operations to accommodate a more digital-centric financial landscape, which could involve restructuring their services and revenue models.

Changes in Monetary Policy Implementation

The introduction of a CBDC like the Digital Rupee could transform how monetary policy is implemented by providing central banks with new tools for influencing the money supply directly through digital channels. With e₹, the Reserve Bank of India (RBI) could conduct monetary policy more effectively by enabling real-time tracking of money flows and enhancing its ability to manage liquidity in the economy. This capability could lead to more responsive monetary policy adjustments based on immediate economic conditions, allowing for greater control over inflation and economic stability. Furthermore, the digital nature of e₹ may facilitate better data collection on spending patterns, enabling the RBI to refine its macroeconomic strategies and improve overall financial governance.

International Implications of CBDCs

Global Trends in CBDC Adoption

Countries worldwide are increasingly exploring Central Bank Digital Currencies (CBDCs), with 87 nations representing over 90% of global GDP currently investigating their potential. This trend has been accelerated by shifts in payment habits towards digital and contactless transactions, particularly following the COVID-19 pandemic, which highlighted the need for modernized financial systems. Notably, nine countries have fully launched state-owned digital currencies, including Nigeria's eNaira and Jamaica's JAM-DEX. As nations refine their CBDC pilots, India's approach to the Digital Rupee will be closely observed as a potential model for other countries considering similar initiatives.

Effects on the International Monetary System

India's adoption of the Digital Rupee could significantly influence global finance by reshaping cross-border payment systems and international trade dynamics. The introduction of a CBDC may facilitate more efficient and cost-effective international transactions, reducing reliance on traditional banking intermediaries. This change could enhance liquidity management and streamline settlements in global markets. As countries like India adopt digital currencies, it may encourage others to follow suit, leading to a more interconnected financial ecosystem that leverages digital currencies for international trade and remittances.

Pilot Projects and Implementation Phases

Image Source: licdn.com

Overview of Pilot Testing Initiatives

The Reserve Bank of India (RBI) has initiated pilot projects to test various aspects of the Digital Rupee (e₹) before full-scale implementation. The first pilot for the Retail Digital Rupee (e₹-R) was launched on December 1, 2022, in a closed user group comprising selected customers and merchants across five cities: Mumbai, New Delhi, Bengaluru, Bhubaneswar, and Chandigarh. This pilot aims to evaluate the functionality and user experience of the digital currency while ensuring that it replicates the features of physical cash, such as trust and settlement finality. The e₹-R is issued in denominations similar to existing paper currency and is distributed through participating banks, including major institutions like the State Bank of India, ICICI Bank, and others.

Lessons Learned from Early Trials

Insights gained from these early trials will inform future developments and help address challenges before a wider launch. The RBI has identified areas for improvement based on user feedback and operational data collected during the pilot phases. For instance, as of early 2023, the retail pilot had reached over 50,000 users and 5,000 merchants, indicating a growing acceptance of the Digital Rupee among participants.

The RBI aims to expand the scope of these pilots gradually, including more banks, users, and locations based on feedback received during initial testing phases. This iterative approach allows for adjustments to be made in real-time, ensuring that the Digital Rupee meets the needs of its users effectively.

Emerging Payment Trends in India (2025)

Key Payment Trends Shaping the Future

As we move into 2025, several emerging payment trends are set to shape how consumers transact in India. Notable among these trends is the explosive growth of the Unified Payments Interface (UPI), which has revolutionized digital transactions by offering a seamless and user-friendly experience. UPI's integration with new technologies, such as conversational voice payments and biometric authentication, is expected to further enhance transaction convenience and security. Additionally, the rise of contactless payments will continue to influence consumer behavior, making transactions quicker and more efficient.

Role of UPI and Mobile Wallets in Transformation

The Unified Payments Interface (UPI) has played a transformative role in India's payment landscape. Its ability to facilitate instant peer-to-peer transactions has made it a cornerstone of digital payments in the country. As UPI evolves, its potential integration with digital currencies, including Central Bank Digital Currencies (CBDCs), could significantly enhance transaction efficiency across platforms. This integration would enable users to make payments using e₹ alongside traditional payment methods, streamlining the user experience and promoting broader adoption of digital currencies.

Moreover, the increasing popularity of mobile wallets is contributing to this transformation. With projections indicating that mobile wallet users in India could reach 900 million by 2025, these platforms are becoming essential for everyday transactions. The synergy between UPI and mobile wallets is expected to create a more interconnected payment ecosystem, facilitating smoother transactions for consumers and businesses alike.

DigiDhan Mission and Its Impact

Image Source: cdfi.in

Overview of the DigiDhan Mission

Launched by the Indian government in June 2017, the DigiDhan Mission aims to promote cashless transactions through various awareness campaigns and initiatives. Under the Ministry of Electronics and Information Technology (MeitY), this mission was established to facilitate a seamless digital payment experience for all citizens, thereby fostering a less cash-dependent economy. The DigiDhan Mission encompasses several innovative initiatives, including the creation of a Digital Payments Dashboard, awareness programs, and incentive schemes designed to enhance access and adoption of digital payments across diverse user segments.

Achievements in Promoting Digital Payments

The DigiDhan Mission has successfully increased awareness about digital payments among citizens, resulting in a remarkable 11-fold growth in digital transactions from 2017 to 2023. This growth is attributed to various initiatives that have improved accessibility and user engagement with digital payment platforms. For instance, the introduction of UPI 123Pay has expanded access to digital payments for feature phone users, while campaigns like DigiShala have helped educate rural populations about digital transactions.

As of early 2024, the mission has recorded over 14,888 crore transactions in the current financial year alone, indicating a significant shift towards digital financial practices among consumers and merchants alike. The mission's emphasis on building customer-centric use cases and enhancing digital literacy has contributed to sustainable habit formation for digital payments.

Conclusion

This discussion has explored various facets surrounding India's journey towards adopting digital currencies, highlighting initiatives such as BIMCOIN and the implications posed by the Digital Rupee (e₹) on traditional banking systems. We examined the DigiDhan Mission, which has significantly increased awareness and adoption of digital payments across demographics, and reviewed the technological advancements underpinning these initiatives. The potential for financial inclusion, transaction efficiency, and the impact on international monetary systems were also key focal points.

Properties for Rent in GurugramProperties for Rent in DelhiProperties for Rent in FaridabadProperties for Rent in KolkataProperties for Rent in PuneProperties for Rent in Greater NoidaProperties for Rent in JaipurProperties for Rent in AhmedabadProperties for Rent in BengaluruProperties for Rent in Lucknow

Properties for Rent in GurugramProperties for Rent in DelhiProperties for Rent in FaridabadProperties for Rent in KolkataProperties for Rent in PuneProperties for Rent in Greater NoidaProperties for Rent in JaipurProperties for Rent in AhmedabadProperties for Rent in BengaluruProperties for Rent in Lucknow